Scaling electronics manufacturing in India presents a complex yet promising trajectory. The industry faces significant hurdles, including import dependencies and a shortage of skilled talent, which limit its growth potential. However, these challenges are counterbalanced by a vibrant ecosystem characterized by rapid domestic expansion, strategic policy initiatives, and increasing global collaborations. To unlock the sector's full potential and secure a competitive edge in a rapidly evolving market, businesses must address these critical bottlenecks and leverage emerging opportunities for innovation and growth.

A Glimpse of India’s Electronics Ecosystem

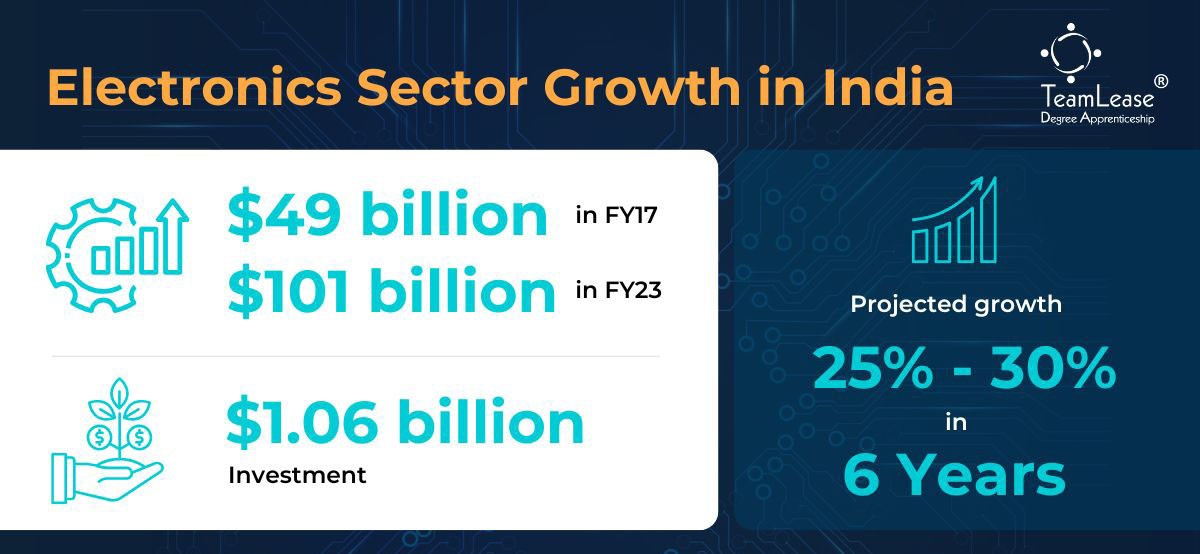

India's electronics industry has witnessed remarkable progress, with domestic production surging from $48 billion in FY17 to $101 billion in FY23. Mobile phones, constituting 43% of total production, lead the charge, followed by IT hardware, consumer electronics, and auto electronics.The semiconductor sector plays a pivotal role, with consumption projected to grow from $22 billion in 2019 to $110 billion by 2030 at a CAGR of 16%. Investments, including Tata’s chip foundry in collaboration with PSMC and Applied Materials’ $400 million engineering center, showcase India’s ambition to become a global semiconductor powerhouse. Despite these achievements, India’s contribution to the global electronics value chain remains under 1%, highlighting the need for strategic interventions to enhance competitiveness and scale.

Key Challenges Confronting the Electronics Industry

While the industry is witnessing a promising growth trajectory, yet it faces critical challenges that hinder its full potential. The industry remains heavily dependent on imports for essential components like semiconductors and PCBAs, driving up production costs and leaving it vulnerable to global supply chain disruptions. Moreover, India struggles to compete with countries like China and Vietnam, which enjoy cost-efficient infrastructure and economies of scale, further complicating its efforts to establish dominance in the sector. A significant talent gap in advanced electronics design and manufacturing exacerbates these issues, stifling innovation and scalability at a time when global demand for cutting-edge technology solutions is on the rise.

Despite these challenges, the sector is teeming with opportunities that position India as a critical player in the global electronics landscape. Strategic investments in electronic manufacturing clusters and collaborations with global technology leaders are bolstering India’s semiconductor capabilities and expanding its footprint in international supply chains. Initiatives like "Make in India," the National Policy on Electronics (NPE) 2019, and incentive-driven programs such as the PLI scheme and EMC 2.0 are fostering an environment conducive to innovation and expansion. Additionally, the "China + 1" strategy is drawing global brands like Apple, Google, and Foxconn to India, not only enhancing manufacturing capacity but also attracting other international players seeking to diversify their supply chains. There is a pressing need to bridge these gaps to ensure sustainable growth and global competitiveness.

Paving the Path to Sustainable Growth

India’s electronics sector must take a holistic approach to achieve sustainable growth, focusing on strengthening domestic manufacturing capabilities, encouraging innovation, and addressing skill gaps. Developing a robust local supply chain for components like PCBAs is critical to reducing import reliance and building a competitive ecosystem. At the same time, expanding ITI programs and increasing capacity from the current 48% will be instrumental in creating a steady pipeline of foundational technical talent.

To meet the demands of a rapidly evolving market, India must also address the growing need for a skilled workforce in advanced manufacturing and semiconductor design. Apprenticeships and work-integrated learning programs provide a practical and scalable solution, aligning education with industry needs while equipping individuals with hands-on experience. These initiatives are essential for preparing the workforce to support the sector’s projected growth, including the anticipated rise in semiconductor consumption from $22 billion in 2019 to $110 billion by 2030.

By combining workforce development with policies like the Production Linked Incentive (PLI) scheme and encouraging a transition to Original Design Manufacturing (ODM) models, India can enhance its competitiveness on a global scale. Apprenticeships, as part of a larger strategy, will play a key role in equipping the nation’s workforce to drive this transformation and secure a prominent position in the global electronics market.

No comments yet

Your Comment